The UK’s deteriorating financial state taking its toll on the advice sector, with rising living costs, spiralling inflation, the long-term impact of lockdowns and Russia’s invasion of Ukraine uniting to create economic turmoil.

While there are myriad ways to measure the impacts these macro events are having on investors and investments, the flow of funds onto and out of platforms is a good indicator. As luck would have it, two such reports have been published on Thursday, with research house Fundscape and consultancy firm The Lang Cat offering similarly glum views on the state of the platform market – albeit by producing, at time, very different figures.

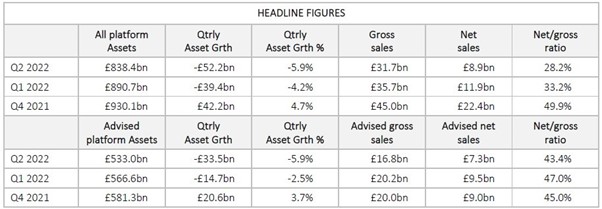

According to Fundscape, total platform assets for Q2 2022 were down 5.9% to £838.4bn ($1.02trn, €991bn). This is a drop of £52.2bn from the previous quarter. In contrast, The Lang Cat saw a 6.62% fall in total platform assets from Q1 2022 but did not provide a total assets figure.

When it came to advised platform assets, The Lang Cat’s latest quarterly platform market scorecard reported a 6.08% decline, while Fundscape data saw assets drop 5.9% to £533bn in the second quarter.

Elsewhere, Fundscape found across all platform channels gross sales suffered a fall to £31.1bn (Q1 2022: £35.7bn), which is a similar outcome for advised gross sales coming in at £16.2bn (Q1 2022: £20.2bn).

Source: Fundscape

In terms of net sales, assets across all platform channels dropped to £8.9bn from £11.9bn the previous quarter, and again there was a similar trajectory for advised platform at £7.3bn for Q2 2022, compared to £9.5bn in Q1 2022.

The Lang Cat’s data found gross sales across all channels were down by 5.31% to £27.9bn, while net sales were down 21.17% compared to Q1 2022, totalling £8.92bn. Outflows increased marginally to £18.9bn (Q1 2022: £18.1bn).

The consultancy firm’s scorecard also found advised platforms gross sales were down 8.37% on the previous quarter to £19.38bn, while net sales came in at £8.85bn (-11.57% on Q1 2022).

Investor confidence to hit ‘fresh lows’

Bella Caridade-Ferreira, chief executive of Fundscape, said: ‘The economic outlook is shaky at best, with little prospect of improvement in the short to medium term. With rampant inflation and fuel prices at unsustainable levels, investor confidence and disposable income will shrink to fresh lows.

“Investors and platforms will have to learn to live with the new normal. For platforms, the downturn comes just as they face another huge regulatory hurdle in the shape of Consumer Duty.

“The platforms that survive will be adept at adapting to disruption and diversifying into multi-channel businesses. Consumers will need significant support over the next few years and will expect their finances to be both digital and seamless across a range of products and services.”

Rich Mayor, senior analyst at The Lang Cat, added: “As we expected after last quarter, advisers have been pragmatic in ensuring this year’s subscriptions are utilised in Q2 2022. Sales were muted but still comfortably above pre-pandemic levels. Advisers we’ve spoken with are spending much more time reassuring their existing clients and tweaking financial plans to tackle the deteriorating economic state of the UK.

“We know advice is often a provision of the wealthy, but even the well-off will feel the pinch of inflation and the grim predictions on energy cap rises in October and January next year. It’s hard to see any way to avoid a recession, certainly if things stay on the same course.

“While sales have been resilient, assets have dropped substantially. Across all channels we’ve seen £66.91bn wiped off the platform market since the end of a bumper 2021, and it’s not very often we write that assets are down year-on-year. That in turn affects platforms’ profitability in terms of revenue from charges on assets, which knocks on to shareholder returns. Platforms will be putting their arms round their biggest supporters to try to protect revenue streams.

“If the trend continues for an extended period, which will certainly be the case if we can’t swerve a recession, we will see platforms moving into markets they’ve not been in before to help alleviate the pressure. This quarter’s likely to be the last time we see these sorts of relatively good sales numbers for a long time to come.”

Provider breakdown

Both firms also had differing numbers on the best performing platform providers.

In terms of all platform channels, Fundscape found Aegon (£8.4bn), Hargreaves Lansdown (£4bn), Fidelity (£3.7bn), AJ Bell (£2.6bn) and Transact (£1.9bn) were top five providers for gross sales in Q2 2022.

Top five for net sales were Hargreaves Lansdown at £2bn, which was followed by AJ Bell (£1.6bn), True Potential (£1.4bn), Transact (£1.2bn) and Aviva (£1.1bn).

For the advised channel, Fundscape found True Potential (£1.3bn), Transact (£1.2bn) and Aviva (£1bn) were the top three for net sales in Q2 2022. The Lang Cat however had Multrees (£1.92bn), True Potential (£1.3bn) and Transact (£1.2bn) as the top three for net inflows in Q2 2022.

Lastly, the Lang Cat’s data found that Abrdn had the largest advised assets under administration (AuA) in Q2 2022 at £68.27bn, with Quilter (£65.78bn), Transact (£50.3bn), Fidelity (£44.58bn) and AJ Bell (£44.3bn).

| Platform | Advised channel net inflow Q2 2022 |

| Multrees | £1.92bn |

| True Potential | £1.30bn |

| Transact | £1.20bn |

| Aviva | £1.05bn |

| AJ Bell | £900m |

Source: The Lang Cat

Transact £1.2bn

True Potential £1.30bn

Aviva £1.05bn