Since the publication of the FCA’s Thematic Review into Retirement Income, one topic has dominated our conversations with clients: do we need a dedicated risk tolerance assessment that focuses on decumulation?

The answer, in short, is ‘no’. However, the importance of the question extends far beyond the length of its answer. Because understanding why it’s a bad idea to use separate accumulation and decumulation-specific risk tolerance assessments is helpful in clearing up several common suitability misunderstandings.

What does the FCA’s Thematic Review say about risk profiling in accumulation and decumulation?

The review says:

Although, generally, the example questionnaires we saw were clear, with unambiguous questions and descriptions, some were written with an accumulation specific focus. This means customers could be inaccurately profiled and take on risk not in line with their circumstances. In a small number of examples firms had recognised that an accumulation-specific risk profiling approach had limitations and supplemented this with a more detailed discussion about retirement income needs and the need for secure income.

Reading this, it’s easy to see how the idea arises that you may need separate accumulation and decumulation-specific risk tolerance assessments.

This, however, would be a misinterpretation of both the specific retirement income issues the review is trying to tackle, and more generally what it means to give suitable advice.

It all starts with an ongoing misunderstanding of what actually constitutes a ‘risk profile’.

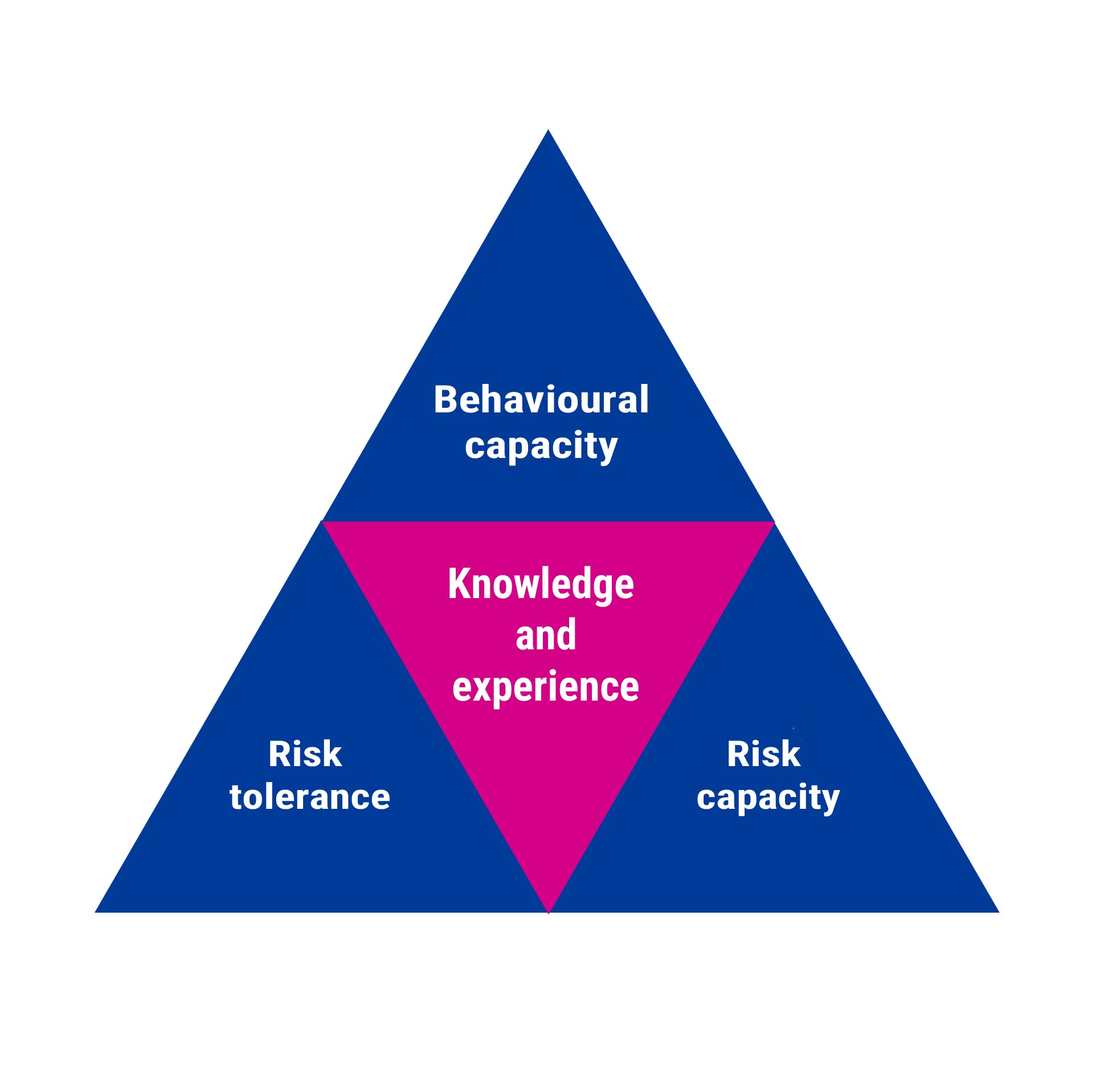

1. Risk tolerance is only one element of a risk profile

An investor’s ‘risk profile’ is the right amount of investment risk for them to take with their investible assets, accounting for their overall financial situation and financial personality.

However, an investor’s risk profile is still mistakenly (and all-too-commonly) seen as interchangeable with their risk tolerance – their willingness to take that risk (which doesn’t reference their ability to take that risk). Ambiguous references to a ‘risk profiling approach’ can therefore be confused with a ‘risk tolerance questionnaire’.

Willingness to take risk (as reflected in risk tolerance) is only one element of an investor’s risk profile. Their financial ability to take that risk, as reflected in their Risk Capacity, is often more important. Their knowledge and experience and emotional ability to take risk (their behavioural capacity) also have crucial roles to play. The mistake is so common, and its consequences so potentially poor, that at Oxford Risk we tend to avoid the term ‘risk profile’ altogether, preferring ‘suitable risk level’

2. The suitable level of risk to take requires consideration of financial circumstances, not just risk tolerance

An investor’s risk profile will likely change on retirement, quite possibly dramatically. In many ways how they see the world is changing. Their advice needs are therefore obviously changing too. But this is because of likely changes in the other elements of their risk profile, not their risk tolerance.

Their income will change.

Their expenditure will likely change too.

Their goals will probably change.

Their major assets may change – eventually, if not immediately.

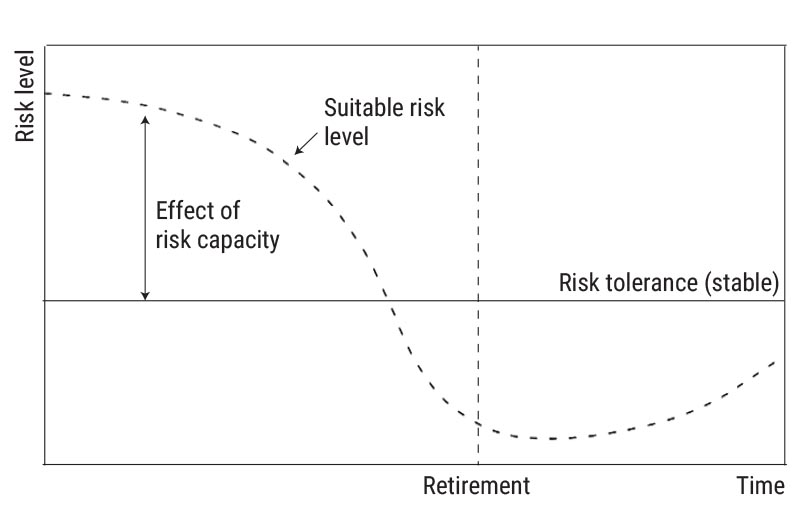

These are all reflected in changes to their risk capacity. Risk capacity reflects an investor’s financial circumstances and is therefore inherently dynamic, at every stage of an investor’s journey. Risk tolerance, by contrast, is a personality trait. It’s connected to who a person is, not what stage of working life they’re moving through. There is no good reason to change how you measure a personality trait from one day to the next because the person being assessed is no longer going to work each morning.

Even if ‘risk profile’ is not seen as fully interchangeable with ‘risk tolerance’, it’s still often (and still mistakenly) seen as predominantly determined by it. However, as the stylised graph above demonstrates, the suitable level of risk for an investor to take might never be the same as their risk tolerance!

Early in life, where the investor has decades of net saving (accumulation) ahead of them, their capacity to take risk with their investible assets is high. But as they approach retirement this changes dramatically: they no longer have a future of net savings, but of withdrawals and net spending (decumulation).

Oxford Risk’s Risk Capacity Assessment was designed to function on both sides of the accumulation/decumulation dividing line – to account for all relevant financial circumstances, and consequently assess how reliant an investor is on their investible assets to fund their future expenditure. It seamlessly accounts for the transition between accumulation and decumulation by fully accounting for changing circumstances.

It’s important to note here that the FCA more commonly refers to ‘capacity for loss’ than ‘risk capacity’. ‘Capacity for loss’ is a narrower concept, fully contained within the broader notion of risk capacity. The FCA’s May 2011 guidance states:

Taken at face value, this definition of ‘capacity for loss’ can only really apply to investors near to, at, or post retirement. If your income covers all your expenditure whilst you’re accumulating early in life then you could lose all your investible assets without any ‘materially detrimental effect’ on your standard of living. This is clearly far too narrow a view to hold for suitable advice, which should be considering changing financial circumstances both in accumulation and decumulation.

3. There are many ways to mess up a Risk Tolerance Assessment, and lack of clarity in the questions is only one of them

In the quote at the top of this article, the FCA notes that it’s possible for questionnaires to be ‘clear, with unambiguous questions and descriptions’ and yet still ‘customers could be inaccurately profiled and take on risk not in line with their circumstances.’

We hope this would be obvious, but in practice, it appears not. Questions being ‘clear’ and ‘unambiguous’ is part of what makes a good Risk Tolerance assessment. But only part! It’s a hygiene factor. Unclear and ambiguous questions is one of a dozen common mistakes we highlight here. The other 11 are also important!

4. Good risk tolerance questions apply equally well to accumulating and decumulating investors

It’s possible by now to be thinking that while accumulation or decumulation-specific questions aren’t necessary, they’re still better. This would also be wrong.

Accumulation-specific questions, however clear they are, and however well-supported they are by supplementary discussion, are unlikely to be measuring Risk Tolerance very well.

If a question has an accumulation focus, it’s highly likely to be confounding the measurement of risk tolerance – a stable, long-term, personality trait – with something more circumstantial. This makes the question ill-suited to a risk tolerance assessment.

The conclusion to draw from this is not that you need separate accumulation and decumulation-specific risk tolerance questions, but that you need questions where the distinction doesn’t matter. Good risk tolerance assessments should be neither accumulation, nor decumulation, specific.

The answer also isn’t to abandon the questions and rely more heavily on subjective discussions. Supplementary discussions around risk profiling are clearly important, especially in terms of how well a client understands why such assessments matter, which can contribute to their engagement with and overall experience of their investing journey. However, outputs of assessments should be inputs into a discussion, not the other way around.

Good suitability methodologies are designed to account for changes in life circumstances, not to be reactively shaped by them

At Oxford Risk, we’ve been talking about these issues and building a methodology and tools to deal with them, for many years. (See, for example, our multi-part response to the FCA’s Call for Input on Consumer investments).

We launched our Risk Capacity Assessment in 2018, and have been refining it ever since. The unique approach it’s built on is the key to helping advisers ensure that their recommendations remain robustly suitable throughout their clients’ transition between accumulation and decumulation.

Greg B Davies, PhD, is head of behavioural finance at Oxford Risk